Baymark Partners Lawsuit: The Real Case Explained

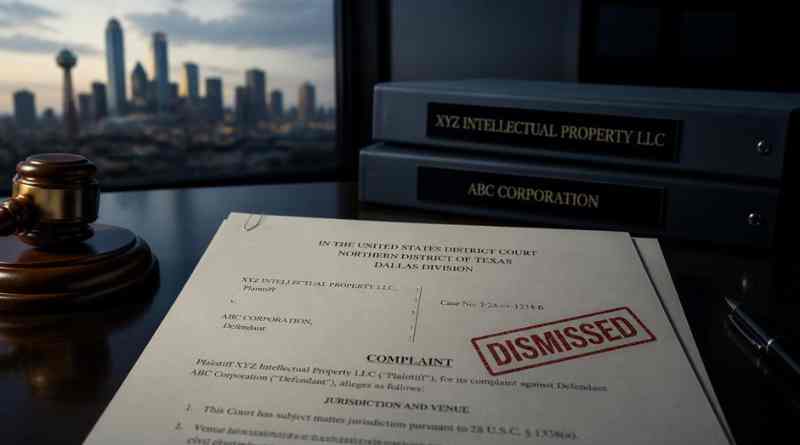

The baymark partners lawsuit refers to D&T Partners, LLC v. Baymark Partners, LP, a RICO and fraud case filed in the U.S. District Court for the Northern District of Texas under Case No. 3:21-cv-01171, alleging that Dallas-based private equity firm Baymark Partners used shell entities, a manipulated lending arrangement, and a fraudulent bankruptcy to steal a company’s assets after acquiring it. The district court dismissed the case with prejudice in 2022, and the Fifth Circuit Court of Appeals affirmed that dismissal in 2024, ruling that while the allegations described coordinated misconduct, they did not meet the legal threshold required to establish a pattern of racketeering activity under the federal RICO statute. As of June 2026, there is no active federal RICO case against Baymark Partners, though the plaintiffs retain the theoretical ability to pursue state law claims separately.

Critically, this case has nothing to do with BayMark Health Services, a completely different company that operates addiction treatment centers and is currently involved in a separate 2024 data breach lawsuit and a 2026 private equity restructuring dispute. This article disentangles both companies, covers the full verified history of the D&T Partners case, and explains exactly what each entity’s legal situation actually involves.

Two Different Companies With Nearly Identical Names

Before covering either case in detail, the most important fact for anyone researching the baymark partners lawsuit is understanding that there are two separate, unrelated companies with confusingly similar names generating search results under this topic.

Baymark Partners, LP is a Dallas-based private equity firm that acquires small and mid-sized businesses, including e-commerce and online retail companies. This is the company involved in the D&T Partners RICO litigation that forms the primary subject of this article.

BayMark Health Services is an entirely separate organization and is reportedly the largest provider of substance use disorder treatment and recovery services in North America, providing services to more than 75,000 patients daily across 35 U.S. states and three Canadian provinces. BayMark Health Services experienced a confirmed data breach in 2024 and is separately the subject of a 2025-2026 private equity restructuring and creditor dispute connected to its own corporate ownership structure.

These two organizations are not affiliated. Confusing them, which several content websites covering this topic have done, produces inaccurate and misleading information. The remainder of this article addresses each company’s legal situation separately and clearly labeled.

The D&T Partners v. Baymark Partners Case: What Actually Happened

The core baymark partners lawsuit began when D&T Partners, LLC, the owner of a successful online retail e-commerce business, was approached by Baymark Partners with an acquisition offer.

According to court filings, Baymark proposed to purchase D&T’s business assets in exchange for cash and a multimillion-dollar promissory note. To complete the transaction, Baymark created a new company, ACET Global, LLC, to take over operational control from D&T, hold the transferred assets, and make payments on the substantial promissory note that was central to the deal structure.

As part of the arrangement, D&T agreed to subordinate its security interest, meaning its legal claim on the company’s assets in case of default, to another lender, identified in court documents as Super G3 or Super G Capital. D&T agreed to this subordination specifically because Baymark had assured D&T that the company’s former management team would remain in control of operations at the newly formed ACET Global.

According to the complaint, those assurances did not last. Less than a year after the sale closed, the plaintiffs alleged that Baymark reneged on its commitments. Baymark allegedly replaced ACET Global’s CEO with what the complaint described as an alleged crony of Baymark’s, who reportedly accepted the new leadership role without compensation. The plaintiffs alleged this leadership change was part of a broader scheme in which Baymark caused the company to default on its loan obligations and then transferred the company’s assets to yet another entity, identified in court records as Windspeed Trading, LLC.

D&T Partners and ACET Global filed suit, alleging that Baymark Partners Management, LLC and a group of associated individuals and entities had attempted to steal the assets and trade secrets of their e-commerce company through a combination of shell entities, what the complaint characterized as corrupt lending practices, and a fraudulent bankruptcy filing.

The Defendants Named in the Case

The lawsuit named a substantial group of defendants beyond Baymark Partners, LP itself, reflecting the complexity of the corporate and lending structure that D&T alleged was used to execute the scheme.

The defendants included multiple Baymark-affiliated entities: Baymark Partners, LP, Baymark Partners Management, LLC, and Baymark ACET Holdco, LLC. Individual executives named as defendants included David Hook, Tony Ludlow, Matthew Denegre, William Szeto, and Marc Cole, among others. Additional parties named in the litigation included Super G Capital and SG Credit Partners, the lenders involved in the loan and security interest arrangements described in the complaint, as well as the law firm Hallett & Perrin.

This wide net of defendants, spanning private equity entities, individual executives, and lending institutions, reflects the scale and complexity of the alleged scheme as described in D&T’s original complaint, which reportedly ran to 194 pages.

The District Court Proceedings: Default Judgment Denied, Claims Dismissed

The case proceeded through several significant procedural stages in the Northern District of Texas before Judge Jane J. Boyle.

Plaintiffs initially attempted to secure a default judgment against Baymark Partners, LP after the entity failed to respond to the complaint. However, the court denied this motion after discovering that Baymark Partners, LP’s certificate of partnership had actually been canceled back in 2012, meaning the entity legally no longer existed as a valid legal party capable of being sued in that form at the time the suit was filed. On June 1, 2022, the court’s memorandum opinion and order formally dismissed the plaintiffs’ claims against the defunct Baymark Partners, LP entity specifically, while other claims against the remaining defendants continued.

In October 2022, the district court issued its more substantive ruling, dismissing the RICO claims with prejudice, meaning they could not be refiled in the same form, and separately dismissing the state law claims, including fraud and breach of fiduciary duty allegations, citing a lack of jurisdiction once the federal RICO claims were no longer part of the case.

The Appeal: Fifth Circuit Affirms Dismissal in 2024

D&T Partners and ACET Global appealed the dismissal to the United States Court of Appeals for the Fifth Circuit, docketed as Case No. 22-11148.

The Fifth Circuit’s ruling, issued in 2024, affirmed the district court’s dismissal. The appellate court’s reasoning centered on a specific and technical element of federal RICO law: the requirement that a plaintiff demonstrate a pattern of racketeering activity, which requires showing a sufficient degree of continuity, breadth, and variety in the alleged criminal conduct, not merely a single scheme directed at a single objective.

The Fifth Circuit held that while D&T’s complaint did allege coordinated theft and misconduct, the alleged victims were limited in number and the scope and nature of the scheme was finite and focused on a singular objective, the acquisition and subsequent asset stripping of D&T’s specific business. This narrow, single-target structure, the court held, did not satisfy the closed-end continuity requirement that RICO’s pattern element demands, which generally contemplates conduct extending over a substantial period of time and affecting multiple distinct victims or schemes.

The court also addressed D&T’s argument that it should have been granted leave to amend its complaint rather than having the case dismissed with prejudice. The Fifth Circuit rejected this argument, noting that while leave to amend should generally be freely given under the Federal Rules of Civil Procedure, D&T’s argument failed to engage with the district court’s several specific, substantive reasons for dismissing the complaint with prejudice in the first place.

The Fifth Circuit’s opinion also addressed and distinguished two other RICO cases D&T had cited as supporting precedent, finding that one case’s complaint, also exceeding 190 pages, hardly described the alleged similarities or underlying predicate acts comparable to D&T’s allegations, and that the other case D&T cited involved healthcare fraud, an issue the court found wholly unrelated to the claims at issue in the D&T complaint.

What the Dismissal Does and Does Not Mean

The Fifth Circuit’s 2024 ruling affirming dismissal of the federal RICO claims is a significant legal outcome, but it is important to understand precisely what this dismissal does and does not establish.

The dismissal does not mean the appellate court found that the underlying alleged conduct was acceptable or that Baymark Partners did nothing wrong. The ruling was a technical, legal determination that the specific federal RICO statute, with its specific and demanding pattern requirement, was not the correct legal vehicle for the claims as D&T had structured and pled them. RICO has notoriously demanding pleading standards, and courts have frequently emphasized that RICO is not meant to serve as a substitute for more traditional fraud or breach of contract claims that may otherwise be available under state law.

As one legal commentator characterized the broader pattern reflected in this ruling, courts continue to signal that they will not allow RICO to substitute for more traditional fraud or contract claims, even where the underlying allegations, if true, describe genuinely serious misconduct.

Because the RICO dismissal was with prejudice, those specific federal racketeering claims cannot be refiled. However, the state law claims, including fraud and breach of fiduciary duty, were dismissed without prejudice and for lack of jurisdiction once the RICO claims fell away, not on their substantive merits. This procedural distinction means the plaintiffs theoretically retain the ability to bring those state law claims in an appropriate state court, where federal RICO’s demanding pattern requirement would not apply.

As of the most recent available legal commentary reviewed for this article, there is no significant new filing confirmed since the Fifth Circuit’s 2024 dismissal. There are currently no active federal RICO cases pending against Baymark Partners, though legal exposure through state court claims remains a theoretical possibility that has not been confirmed as pursued.

What Happened to ACET Global

A notable postscript to the underlying dispute involves ACET Global, the entity Baymark created to hold and operate the acquired D&T assets. According to court filings referenced in subsequent legal commentary, ACET Global filed for bankruptcy shortly after the asset transfers that D&T alleged were part of the broader scheme, with court filings in that bankruptcy proceeding that allegedly contained misrepresentations about the company’s financial condition.

This bankruptcy filing is part of why the underlying dispute is sometimes described in legal commentary as involving a fraudulent bankruptcy, referring to the allegation that the bankruptcy itself was used as a tool within the broader scheme to finalize the transfer of value away from the original D&T ownership structure, rather than as a good-faith response to genuine insolvency.

Lessons for Business Owners Considering a Private Equity Sale

Legal commentary on the D&T Partners v. Baymark Partners case has consistently drawn broader lessons applicable beyond this specific dispute, relevant to any business owner considering a sale to a private equity acquirer.

Transparency in financial dealings and entity structuring is critical for private equity firms operating in this space, and the use of shell entities or rapid shifting of assets between newly created subsidiaries can spark serious legal challenges, even when those challenges do not ultimately succeed under specific statutes like RICO.

For business owners selling to a private equity buyer, protecting your rights through carefully negotiated contracts, properly secured security interests, and ongoing monitoring of the acquiring entity’s conduct after closing is essential. D&T’s experience illustrates the risk of accepting verbal or informal assurances, such as a promise about ongoing management control, that are not adequately secured through binding contractual terms enforceable independent of the new owner’s good faith.

For creditors and lenders involved in financing acquisitions of this type, the case illustrates the complexity that can arise when subordination agreements and security interests are negotiated based on representations that the acquiring party later does not honor.

The Separate BayMark Health Services Situation

Distinct from the Baymark Partners litigation discussed above, BayMark Health Services, the addiction treatment company, has its own separate and unrelated legal and corporate developments worth understanding if you encountered this name in your research.

In a confirmed data breach, an unauthorized party gained access to some of BayMark Health Services’ IT systems between September 24, 2024 and October 14, 2024. By November 5, 2024, it was determined that the exposed files contained sensitive patient information, including names, Social Security numbers, driver’s license numbers, birth dates, treatment and service details, insurance data, and diagnosis information. BayMark began notifying affected patients on January 8, 2025. Class action attorneys subsequently opened an investigation into this breach, seeking to represent affected patients in claims for loss of privacy, time spent addressing the breach, and out-of-pocket costs.

Separately, BayMark Health Services has been the subject of 2025-2026 reporting on private equity sector restructuring, following a 2024 bankruptcy filing involving financial misrepresentation claims connected to its ownership and financial reporting. This situation involves a dispute between private equity sponsors seeking an exit from their investment and creditors pursuing recovery of value, centered on disagreements over approximately $75 million in marketed earnings figures. This restructuring story is fundamentally a corporate finance and creditor dispute distinct from any RICO or fraud litigation and has no direct legal connection to the Baymark Partners, LP entity discussed throughout the rest of this article.

If you are researching this topic because you are a patient affected by the BayMark Health Services data breach, that is a separate matter from the Baymark Partners private equity litigation, and you should specifically search using the full BayMark Health Services name and reference the September-October 2024 breach period when seeking information or legal consultation.

Frequently Asked Questions

What is the baymark partners lawsuit?

It refers to D&T Partners, LLC v. Baymark Partners, LP, Case No. 3:21-cv-01171, filed in the U.S. District Court for the Northern District of Texas. D&T Partners alleged that Baymark Partners, a Dallas private equity firm, used shell entities, manipulated lending arrangements, and a fraudulent bankruptcy to steal D&T’s business assets after acquiring the company. The case was dismissed and the dismissal was affirmed by the Fifth Circuit Court of Appeals in 2024.

Who won the Baymark Partners lawsuit?

The Fifth Circuit Court of Appeals affirmed dismissal of D&T’s RICO claims in 2024, ruling that the allegations, while describing coordinated misconduct, did not meet the legal threshold for a pattern of racketeering activity required under federal RICO law.

Is there an active lawsuit against Baymark Partners right now?

No active federal RICO case against Baymark Partners is confirmed as of June 2026. The RICO claims were dismissed with prejudice and cannot be refiled. The state law claims were dismissed without prejudice for lack of jurisdiction, meaning they theoretically could be pursued in state court, though no confirmed new filing has been identified.

Is Baymark Partners the same company as BayMark Health Services?

No. These are two completely separate and unrelated companies. Baymark Partners, LP is a Dallas-based private equity firm involved in the D&T Partners litigation. BayMark Health Services is the largest substance use disorder treatment provider in North America and is involved in a separate 2024 data breach lawsuit and unrelated 2026 corporate restructuring dispute.

What happened to ACET Global, the company Baymark created?

ACET Global, the entity Baymark created to hold D&T’s transferred assets, filed for bankruptcy shortly after the alleged asset transfers, with court filings that allegedly contained misrepresentations about the company’s financial condition.

How much money was involved in the Baymark Partners lawsuit?

Court documents indicate ACET Global owed D&T Partners a promissory note worth several million dollars, with allegations involving the theft and transfer of assets valued in the millions of dollars.

Final Word

The baymark partners lawsuit is a real, fully documented federal case, D&T Partners, LLC v. Baymark Partners, LP, that ended in dismissal at both the district court and Fifth Circuit appellate level, on the specific technical grounds that the alleged conduct did not satisfy RICO’s demanding pattern of racketeering activity requirement. The underlying factual allegations, involving shell entities, a broken management promise, asset transfers, and a contested bankruptcy, remain serious and were never substantively disproven; they simply did not fit the particular federal statute D&T chose to pursue them under.

Separately, and importantly, BayMark Health Services is a different company entirely, with its own distinct and unrelated legal situation involving a 2024 patient data breach and an ongoing 2026 private equity restructuring dispute. Anyone researching either topic should be careful to confirm which specific entity and which specific case applies to their situation before drawing conclusions or taking action.

Note: This article is for informational purposes only and does not constitute legal advice. Consult a licensed attorney for guidance specific to your situation.