Santander Consumer Western Avenue Nissan Lawsuit Guide

The santander consumer western avenue nissan lawsuit is a RICO class action filed in the U.S. District Court for the Northern District of Illinois in May 2025, bearing Case No. 1:2025cv05106, styled as Burress v. Western Avenue Nissan, Inc. Lead plaintiff Tanisha Burress alleges that Western Avenue Nissan, a Chicago dealership, falsified financial and employment information on customer loan applications submitted to Santander Consumer USA in order to get buyers approved for loans they would not otherwise qualify for. Critically, the lawsuit does not accuse Santander Consumer USA of misconduct. The allegations target the dealership’s conduct specifically. As of June 2026, the case remains active in federal court in Chicago with no class certification ruling and no settlement announced.

What Is Western Avenue Nissan and Why Does This Matter?

Western Avenue Nissan is a car dealership located in Chicago, Illinois, on Western Avenue near the city’s south side. The dealership sells new and used Nissan vehicles and, like most auto dealerships in the United States, arranges financing for customers through third-party lenders rather than lending money directly from its own balance sheet.

This dealer-arranged financing model is the standard operating structure across the American auto industry. A buyer visits a dealership, selects a vehicle, provides financial and employment information, and the dealership packages that information into a loan application submitted to one or more lenders for approval. When the lender approves the application, the lender purchases the loan from the dealer at a slight discount, and the customer repays the lender directly over the life of the loan.

Santander Consumer USA is one of the largest subprime auto loan lenders in the United States, operating from its headquarters in Dallas, Texas. It provides financing primarily to buyers with below-average or limited credit histories, the subprime market, which is exactly the customer population that dealerships like Western Avenue Nissan regularly refer to lenders like Santander. In this arrangement, Santander purchased loan paper from Western Avenue Nissan without originating the loans itself.

The relationship between the dealership and the lender is the precise mechanism through which the alleged fraud in the santander consumer western avenue nissan lawsuit could operate, and it is also the reason why Santander’s name appears in every search result for this case even though the lawsuit itself does not accuse Santander of any wrongdoing.

The Burress Lawsuit: What Tanisha Burress Alleges

In May 2025, Tanisha Burress filed a federal RICO class action complaint against Western Avenue Nissan in the Northern District of Illinois. The case is docketed as Case No. 1:2025cv05106.

The RICO designation, referring to the federal Racketeer Influenced and Corrupt Organizations Act, signals that Burress’s attorneys are alleging not just a single instance of fraud but a pattern of racketeering activity, a series of fraudulent acts conducted through an enterprise in a sufficiently broad and continuous pattern to meet RICO’s demanding legal standard.

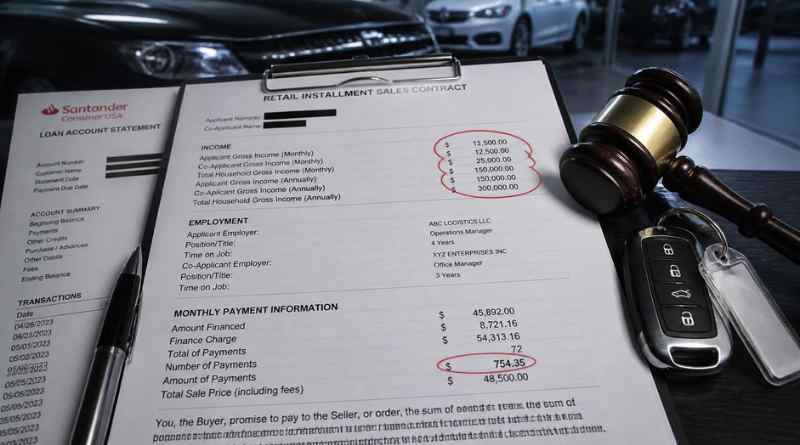

The specific allegations in the complaint describe a practice at Western Avenue Nissan in which dealership staff systematically falsified information on loan applications before submitting them to Santander Consumer USA. The types of falsifications described in the complaint and in industry coverage of the case include the following.

Income figures higher than what buyers actually disclosed to the dealership, making buyers appear more creditworthy than their actual financial situation supported. Employment information changed or fabricated to reflect more stable or higher-paying positions than buyers actually held. Housing payment figures listed lower than buyers’ actual costs, making their monthly financial obligations appear less burdensome. Employment status changed to self-employed when buyers never identified themselves that way. These falsifications, taken collectively, were allegedly designed to ensure that buyers who would not qualify for loan approval under their actual financial circumstances would pass through Santander’s underwriting criteria based on the manipulated numbers.

The result alleged in the complaint is that buyers were approved for high-interest subprime loans, sometimes with interest rates exceeding 20 percent, that their actual income and employment situation would not have supported, placing them in debt obligations they could not realistically sustain.

Why This Is a RICO Case and What That Legal Standard Requires

The RICO designation in the santander consumer western avenue nissan lawsuit is significant because RICO is one of the most powerful and most demanding federal statutes a plaintiff can invoke.

For a RICO claim to survive, the plaintiff must allege and ultimately prove four specific elements. First, the defendant must have conducted or participated in an enterprise, meaning an ongoing organization or group with a common purpose. Second, the defendant must have participated through a pattern, meaning a series of related predicate acts, not just an isolated incident. Third, those predicate acts must be racketeering activity, meaning they must fit within one of the specific categories of criminal conduct that RICO lists, which includes mail fraud, wire fraud, and bank fraud, all of which are potentially applicable to falsified loan application submissions. Fourth, the racketeering must have caused the plaintiff’s injury.

The pattern requirement is where many RICO cases fail, as was discussed in the Baymark Partners case covered separately on this site. Courts require that the predicate acts be related and that they demonstrate a degree of continuity, either by constituting a regular pattern over a substantial period or by posing a threat of future continuation. A single fraudulent transaction at a dealership would not satisfy this standard. A systematic practice of falsifying loan applications for multiple buyers across multiple transactions over an extended period is much more likely to meet the pattern requirement if the evidence supports it.

The class action structure of the Burress filing reflects the legal theory that the pattern was not limited to Burress individually but extended across multiple buyers at Western Avenue Nissan who financed through Santander Consumer USA. If the class is certified, the case would proceed on behalf of all qualifying buyers who obtained Santander-financed loans through the dealership during the class period, typically defined in auto fraud cases as a period of several years covering the alleged scheme.

Why Santander Is in the Search Term But Not the Defendant

The santander consumer western avenue nissan lawsuit creates natural confusion because Santander Consumer USA is so prominent in the search terms, in the news coverage, and in the financial documents that affected buyers hold in their hands.

Every buyer who financed through this arrangement has Santander Consumer USA prominently displayed on their loan agreement, their monthly statements, and in calls from their lender. Santander is the entity that calls them about payments, that holds their loan account, and whose name appears on every financial communication they receive. From the buyer’s experiential perspective, Santander is the company with whom they have an ongoing financial relationship.

But the legal theory in the Burress complaint is that Western Avenue Nissan, the dealer, is the party that falsified the applications before submitting them to Santander. Santander purchased loan paper that the dealership had submitted. The complaint does not allege that Santander knew the applications were falsified or that Santander itself manipulated any information. As multiple credible auto finance legal sources have specifically noted when covering this case, the suit described did not accuse Santander of misconduct.

This lender versus dealer distinction is legally important because the two parties have different exposure, different defenses, and different relationships with the affected buyers. A buyer with a complaint about how their application was processed has a different legal claim than a buyer with a complaint about how their loan was serviced after origination. The Western Avenue Nissan RICO case targets the origination process conducted by the dealership, not Santander’s subsequent loan servicing.

Santander Consumer USA’s Separate Regulatory History

While Santander is not a defendant in the Western Avenue Nissan RICO case specifically, understanding the santander consumer western avenue nissan lawsuit landscape requires acknowledging Santander’s documented separate legal and regulatory history in the subprime auto lending space.

In May 2020, Santander reached a multistate settlement with state attorneys general across multiple states, paying restitution and civil penalties related to allegations about its subprime auto lending underwriting practices dating back to approximately 2010. That settlement involved allegations that Santander had looser-than-appropriate controls over the quality and accuracy of loan applications it purchased from dealers, allowing loans to be approved for borrowers who were likely to default. That settlement addressed Santander’s institutional role in a systemic underwriting problem, not individual dealer conduct.

The Consumer Financial Protection Bureau has also reviewed Santander’s add-on product disclosures, with a CFPB enforcement action related to Santander’s GAP add-on product disclosures having a settlement page last modified January 2, 2024.

These prior Santander regulatory matters are separate from and not legally connected to the Burress v. Western Avenue Nissan case. They involve different time periods, different legal theories, and different factual allegations. However, they provide the broader context of why Santander’s name and subprime auto lending practices have attracted sustained regulatory attention, which in turn helps explain why buyers frequently connect Santander’s name to any auto finance dispute connected to its dealer network.

The Older Related Case: Santander Consumer USA v. Sandy Sansing Nissan

A separate case that appears in searches related to the santander consumer western avenue nissan lawsuit, but which is distinct and unrelated to the Burress filing, is Santander Consumer USA Inc. v. Sandy Sansing Nissan Inc. et al., filed under case number 3:2022cv08084.

This older case is essentially the reverse of the Burress situation. Rather than a buyer suing a dealership for falsifying loan applications, this case appears to involve Santander Consumer USA itself as the plaintiff, suing a Nissan dealership. A court order from June 13, 2022 denied a motion to remand and approved transfer of this case to another federal district. The court’s June 2022 order addressed venue and procedural matters rather than the substantive fraud claims, with those claims to be addressed by the receiving court after transfer.

This older case is not the Western Avenue Nissan situation. The dealership is different, the geographic jurisdiction is different, the parties are in reversed positions, and the case is from 2022 rather than 2025. Understanding this distinction prevents the conflation of two entirely separate cases that occasionally appear together in search results.

What Affected Buyers Should Do Right Now

If you purchased a vehicle from Western Avenue Nissan and financed through Santander Consumer USA, the following steps are appropriate given the current state of the Burress case.

Gather your loan documentation. Collect your original purchase order, the fully executed retail installment sale contract, any add-on product agreements, your loan account statements, and all correspondence with the dealership and with Santander. Compare the financial figures on your executed loan documents with the information you actually provided to the dealership at the time of purchase. If your stated income, employer, income type, or housing payment on the loan document does not match what you actually told the dealership, that discrepancy is legally significant.

Specific warning signs consistent with the allegations in the Burress complaint include an income figure on your loan application that is higher than what you disclosed, an employer name or job title you did not provide, a housing payment listed lower than your actual rent or mortgage, your employment type listed as self-employed when you are not, a co-signer or co-borrower added without your knowledge or consent, and add-on products such as GAP insurance or extended warranties appearing on your final contract that you declined during the sales process.

Contact one of the law firms known to be investigating or handling the Burress case. Edelman Combs Latturner & Goodwin LLC, based in Chicago and reachable at (312) 739-4200, was specifically cited in coverage of this case as accepting inquiries from affected buyers. Most class action attorneys handle initial consultations at no cost and work on contingency, meaning no upfront fees.

File a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov and with the Illinois Attorney General’s consumer protection division at illinoisattorneygeneral.gov. These regulatory complaints do not directly resolve your individual situation, but they contribute to the documented evidentiary record that supports both the regulatory response and the class action litigation.

Monitor the Burress case docket through CourtListener or the federal PACER system. Case No. 1:2025cv05106 in the Northern District of Illinois is publicly accessible. Any class certification ruling, settlement announcement, or significant motion filing will appear on that docket before appearing anywhere else.

Do not accept or sign any confidential settlement offer from Western Avenue Nissan without first consulting a class action attorney. Accepting an individual settlement can constitute a waiver of your right to participate in the class action if the class is later certified.

The Broader Auto Finance Fraud Pattern This Case Represents

The santander consumer western avenue nissan lawsuit does not exist in isolation. It reflects a documented and recurring pattern in the American auto finance industry in which dealership staff falsify loan application information to secure approvals for buyers who would not otherwise qualify under the lender’s underwriting standards.

This practice is economically motivated at the dealership level. A dealer’s profit on a vehicle sale depends on completing the transaction. If a buyer does not qualify for financing at a dealworthy rate, the sale does not happen. Falsifying income or employment information to push an application through underwriting secures the sale and generates the dealer’s profit margin on both the vehicle and the financing. The buyer is left holding a loan obligation built on false premises that may not reflect their actual financial capacity.

The subprime auto market in which Santander operates is particularly vulnerable to this pattern because subprime borrowers are, by definition, buyers whose credit profiles are marginal enough to require extra scrutiny. When dealers manipulate the financial data supporting subprime applications, they exploit the structural gap between what the lender sees on paper and what the buyer’s actual situation is.

Legal consequences for dealerships found to have engaged in this conduct can include RICO penalties, which can be substantial given RICO’s treble damages provision, state consumer fraud damages, and potential criminal referrals for the individuals who executed the falsifications. The class action structure of the Burress filing means that if Western Avenue Nissan’s practices were as systematic as alleged, the aggregate damages across all affected buyers could be significant.

Frequently Asked Questions

What is the santander consumer western avenue nissan lawsuit?

It is a RICO class action, Burress v. Western Avenue Nissan, Inc., Case No. 1:2025cv05106, filed in the U.S. District Court for the Northern District of Illinois in May 2025. Lead plaintiff Tanisha Burress alleges that Western Avenue Nissan falsified financial and employment information on customer loan applications submitted to Santander Consumer USA. The lawsuit does not accuse Santander of wrongdoing.

Does the lawsuit accuse Santander Consumer USA of fraud?

No. The complaint specifically targets Western Avenue Nissan’s alleged conduct in falsifying loan applications before submitting them to Santander. Santander is the lender whose name appears on affected buyers’ loan documents but is not a named defendant accused of misconduct in the Burress case.

Who is Tanisha Burress?

She is the lead plaintiff in the Burress v. Western Avenue Nissan class action, filed in May 2025. She alleges that the dealership provided false financial information on her loan application to secure an unaffordable Santander-financed auto loan.

Is there an open settlement I can file for?

No. As of June 2026, no class has been certified and no settlement has been announced. If a settlement is eventually reached, notice will be sent to class members by a court-appointed claims administrator and announced through official court documents.

How do I know if my loan application was falsified?

Compare the financial figures on your executed loan documents with the information you actually provided to the dealership. Discrepancies in stated income, employer, employment type, housing payment, or the addition of a co-borrower or add-on products you did not select are all potential indicators. Contact a class action attorney for a case-specific evaluation.

What law firms are handling the case?

Edelman Combs Latturner & Goodwin LLC in Chicago at (312) 739-4200 was specifically cited in coverage of the Burress case as accepting inquiries from affected buyers. Initial consultations are typically free and claims are handled on contingency.

Final Word

The santander consumer western avenue nissan lawsuit is a live, active RICO class action in federal court in Chicago targeting a dealership’s alleged practice of falsifying buyer financial information to secure Santander Consumer USA auto loan approvals. The key facts to retain are: the complaint targets Western Avenue Nissan’s conduct, not Santander’s; the lead plaintiff is Tanisha Burress; the case is filed under RICO in the Northern District of Illinois; no settlement or class certification exists yet as of June 2026; and Santander’s name in the search term reflects its role as the lender on affected buyers’ loan documents, not its role as a defendant in this specific case.

If you purchased a vehicle at Western Avenue Nissan and financed through Santander Consumer USA, gather your loan documents, compare figures against what you actually disclosed, consult a class action attorney, and monitor the case docket for developments.

Note: This article is for informational purposes only and does not constitute legal advice. Consult a licensed attorney for guidance specific to your situation.